The COVID-19 pandemic was a wakeup call to Americans. Most people realized we import many of the products we use every day from China and other countries. What Americans did not realize was how dependent we were/are on China and other countries for Personal Protective Equipment (PPE) such as gloves, gowns, masks, face shields and medical equipment. For example: frontline health care workers could not get N-95 masks and essential PPE. Nurses were forced to wear trash bags for protection. There are many stories like this.

Americans lost jobs because of businesses shutting down during the pandemic. Manufacturers were forced to shut down assembly lines because parts of their supply chain were overseas, and those facilities were also impacted by the pandemic. U.S. job losses have been in the millions. Now, more than ever Job creation is a major interest for most Americans.

Since March, when the pandemic started, Shale Crescent USA’s media outreach has increased dramatically. Shale Crescent USA has been radio guests on nationally syndicated and large market stations across the country ranging from New York City to Boston to Chicago to Denver to Los Angeles to Seattle. What we learned from talking to hosts and callers (regardless of political affiliation and regardless of urban or rural location) is Americans want to bring manufacturing and high paying jobs back to the USA. The question that follows is “Can we manufacture in the U.S.?”

Based on the research and expertise of Shale Crescent USA, this paper answers that question.

Introduction:

The U.S. energy advantage has created a significant national opportunity to create high wage U.S. manufacturing jobs. For the past three decades, U.S. manufacturers have migrated overseas to China primarily due to cheaper foreign labor and a decreasing U.S. energy supply. Today, the China labor advantage is steadily deteriorating and the U.S. has an abundant energy supply. The opportunity to onshore manufacturing to the U.S. based on superior economics is the strongest it has been in many years.

Manufacturing jobs are directly tied to the stability and growth of U.S. oil and gas production. Oil and gas are the primary feedstock and fuel supply for many manufacturers. Without oil and gas, modern manufacturing can’t exist. This makes the cost and availability of energy a significant component in the economics of manufacturing.

U.S. Energy and U.S. Manufacturing Directly Correlated:

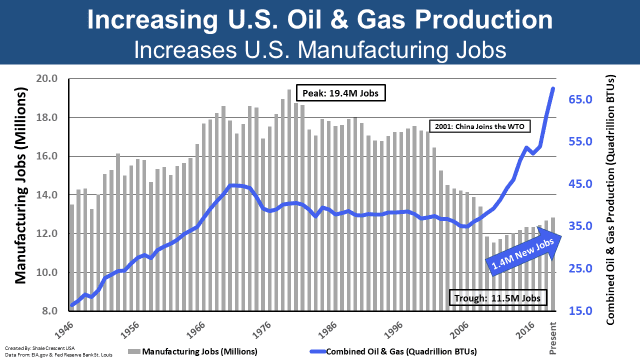

The following chart illustrates the direct correlation of U.S. Oil and Gas Production to U.S. Manufacturing jobs.

As oil and gas production rose, so did the ability to competitively manufacture within the United States. Similarly, as  U.S. Oil and Gas production declined (seen from the mid 1970’s to the early 2000’s), nearly 3 million manufacturing jobs were lost. Another 5 million manufacturing jobs were lost when China joined the WTO in 2001. However, the amount of total jobs lost is actually much larger. For every one manufacturing job created, there are four to five supporting jobs generated. Around 2010, due to shale development, U.S. oil and gas production reversed course and the U.S. quickly became the number one oil gas producing country in the world. As a result, manufacturing jobs began to rebound. Today, there have been 1.4 million manufacturing jobs created since the U.S. shale development.

U.S. Oil and Gas production declined (seen from the mid 1970’s to the early 2000’s), nearly 3 million manufacturing jobs were lost. Another 5 million manufacturing jobs were lost when China joined the WTO in 2001. However, the amount of total jobs lost is actually much larger. For every one manufacturing job created, there are four to five supporting jobs generated. Around 2010, due to shale development, U.S. oil and gas production reversed course and the U.S. quickly became the number one oil gas producing country in the world. As a result, manufacturing jobs began to rebound. Today, there have been 1.4 million manufacturing jobs created since the U.S. shale development.

U.S. Location Advantage:

The current Asia based manufacturing model is: Energy based raw materials are shipped to Asia, they are used to  manufacture goods, and those finished goods are then shipped to the U.S. This model is obsolete. In addition to being the number one oil and gas producing country in the world, the U.S. is also the largest economy in the world. U.S. supply and demand are in the same location. This logistics advantage over other countries creates two primary benefits. 1) Avoidance of the cost of shipping the energy overseas and the cost of shipping the finished product to the U.S. 2) Elimination of emissions from shipping the energy overseas and the finished goods back to America. Utilizing U.S. energy supply to manufacture in the U.S. is both more cost competitive and greener.

manufacture goods, and those finished goods are then shipped to the U.S. This model is obsolete. In addition to being the number one oil and gas producing country in the world, the U.S. is also the largest economy in the world. U.S. supply and demand are in the same location. This logistics advantage over other countries creates two primary benefits. 1) Avoidance of the cost of shipping the energy overseas and the cost of shipping the finished product to the U.S. 2) Elimination of emissions from shipping the energy overseas and the finished goods back to America. Utilizing U.S. energy supply to manufacture in the U.S. is both more cost competitive and greener.

U.S. Manufacturing Competitiveness:

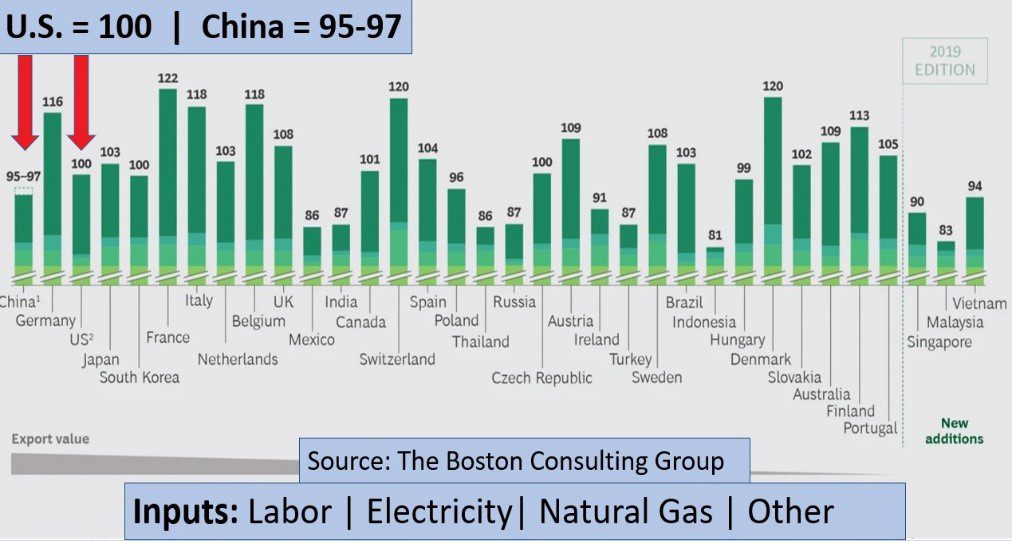

The concept that manufacturing in China is far cheaper than manufacturing in the U.S. is no longer valid. Annual double digit increases in Chinese labor costs and abundant low cost U.S. energy have moved the two countries close to parity. The Boston Consulting Group annually analyzes and compares manufacturing cost competitiveness between  the U.S. and other manufacturing countries. Their 2018 report indicates China’s manufacturing cost advantage over the U.S. has vastly eroded.

the U.S. and other manufacturing countries. Their 2018 report indicates China’s manufacturing cost advantage over the U.S. has vastly eroded.

The United States now has advantages in manufacturing that it has not had for decades. Advanced manufacturing and robotics have made U.S. labor costs more competitive with other regions of the world. Because of America’s history of manufacturing the U.S. has an experienced workforce, hands on training facilities and technical institutions to train new workers. In addition, the U.S. has abundant low-cost energy and feedstocks. If locating in the Shale Crescent USA, manufacturers can take advantage of being in both the center of their feedstock/energy and in the middle of their customers. This further creates economic advantages.

These changes have occurred rapidly and in just the past few years. Many companies do not yet realize the global manufacturing shift and the magnitude of the change. Many Americans may not have been born or remember the Arab Oil Embargo of the 1970s or the energy crisis of the 1990s and early 2000s. They may not realize one of the main reasons U.S. manufacturing jobs were lost was because of the decline in U.S. oil and gas production. For decades, the U.S. has been reliant on getting energy from OPEC. That is no longer the case. Many people may not realize how important oil and natural gas are to manufacturing. They also may not realize renewables only produce one product (electricity) and cannot produce the feedstocks required for manufacturing. Steps must be taken to recapture lost U.S. manufacturing.

Steps to Creating U.S. Manufacturing Jobs:

America’s abundant energy supply has created an opportunity to generate new manufacturing and onshore lost manufacturing. A series of actions should be taken to facilitate this creation of U.S. manufacturing jobs.

- Government Agency Support – Creating a Department of Manufacturing: Currently there is no organization whose primary role is supporting or attracting manufacturing to the U.S.

Focus items:

a. Favorable tax policies to create and/or re-shore manufacturing: Jobs were moved overseas because companies had the significant savings incentives of lower manufacturing (labor) costs. A corporate tax incentive to create U.S. based manufacturing jobs would be beneficial.

b. Transparent and reasonable regulation: To attract investment in the U.S. for manufacturing, U.S. and foreign companies need to know the regulatory process is clear and reasonable; elimination of unnecessary and bureaucratic red tape must continue to be a priority. - Identifying the Opportunities – U.S. Manufacturing Opportunity Study: A study should be conducted identifying imported products which are vital to U.S. interests or products which can now be produced cost competitively in the U.S. A study analyzing, identifying, and inventorying imported products to the U.S. would cover two areas broadly defined as “Should” and “Could”.

a. Should: Products that “should” be made here based on national or corporate strategic importance.

Example: Personal protection equipment and medical devices.

b. Could: Products that “could” be made here based on economic competitiveness.

Example: Toothbrushes – Products made from plastics and where production can be automated. - Strengthening the Argument – Linking Manufacturing to Oil & Gas: A concerted effort should be made to highlight the correlation of the production of oil and gas to manufacturing jobs. The general population must understand U.S. manufacturing jobs are tied directly to the ability to effectively produce U.S. oil and gas.

- Reduced Emissions – Choosing where manufacturing will have the lowest environmental impact. When a product is produced and consumed in the U.S., there are lower emissions and a smaller carbon footprint than if that item was imported. By 2050, our planet will have an additional 2 billion people to feed, clothe, house, and provide jobs for work. Demand for products made from petrochemicals and plastics will continue to increase.

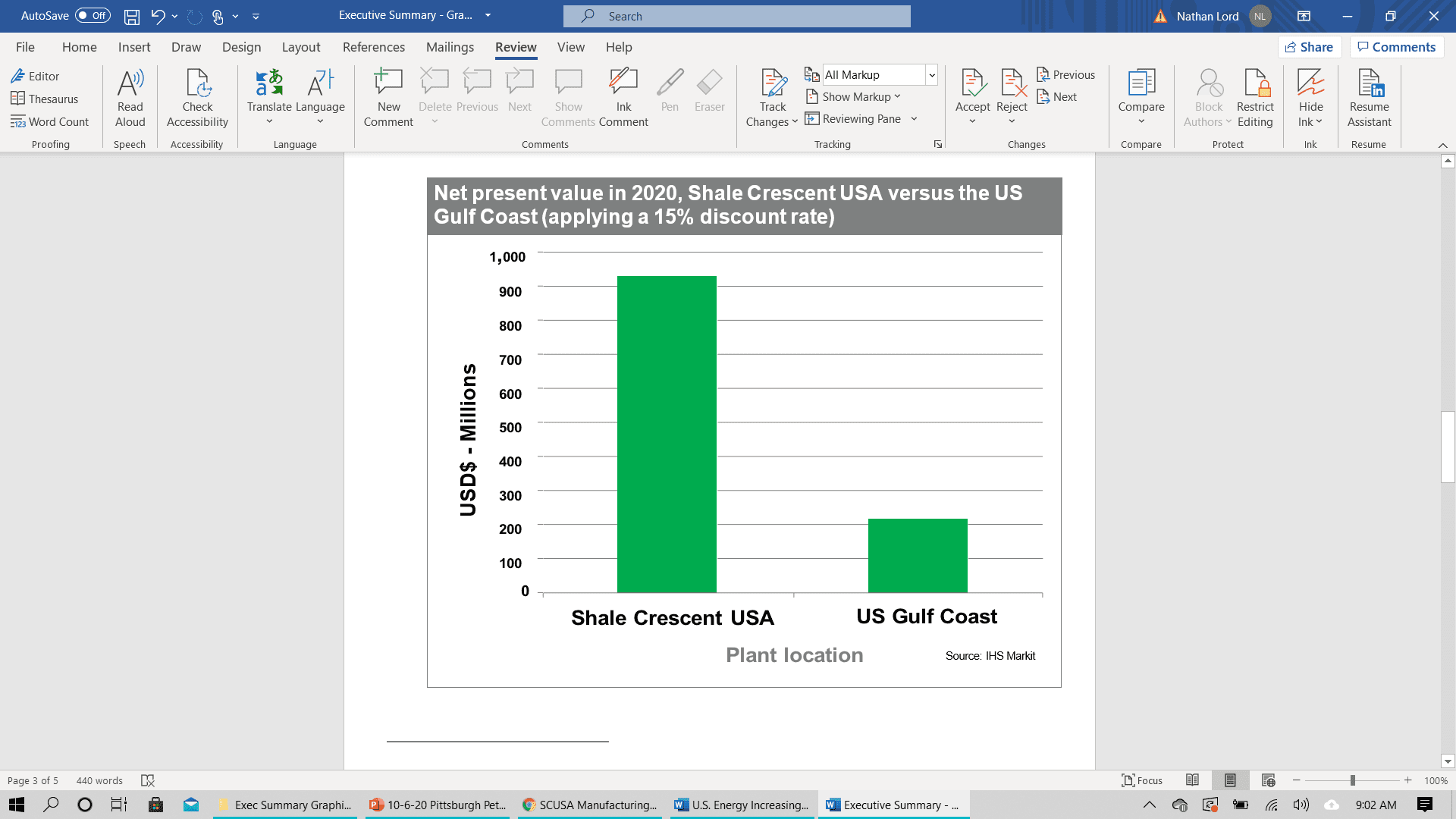

- Awareness – How the world has changed and the new opportunities within the industry that have been created. The change in the United States from energy crisis to energy leader occurred in about 10 years. In March 2018 at the World Petrochemical Conference in Houston, the IHSMarkit/Shale Crescent USA study was released. The study, Benefits, Risks, and Estimated Project Cash Flows: Ethylene Project Located in the Shale Crescent USA versus the US Gulf Coast was presented from the main stage. This report compared the risks of a major petrochemical and plastics investment in the Shale Crescent USA Region with an identical investment in the US Gulf Coast. The US Gulf Coast currently leads the world in petrochemical manufacturing expansion. The bottom-line results were:

The expected financial returns for a Shale Crescent USA project compared with a Gulf Coast project are higher under all analyzed price scenarios, and these results are robust when considering a range of capital cost, operating rate conditions, and domestic/international sales scenarios.The comparative financial advantage for a Shale Crescent project would be further enhanced if more-than- anticipated transportation and natural gas and NGL storage and pipeline infrastructure development occurs in the region.

This study and the Boston Consulting Group Report are less than 3 years old. It will take time and a marketing effort for this information to widely reach industry leaders in manufacturing, petrochemicals, and finance. However, development within the region is well underway.

This study and the Boston Consulting Group Report are less than 3 years old. It will take time and a marketing effort for this information to widely reach industry leaders in manufacturing, petrochemicals, and finance. However, development within the region is well underway.

U.S. and foreign companies have begun looking seriously at the Shale Crescent USA region. The Shell Pennsylvania Petrochemical Complex is under construction in Pennsylvania, while a second cracker plant is under-consideration by PTT Global Chemical in Belmont County, Ohio. The pieces to a positive, yet still widely unknown, opportunity continue to come together in the Shale Crescent USA region.

In-Summary:

Historically, manufacturing jobs have been directly tied to the stability and growth of U.S. oil and gas production. America’s abundant energy supply and world class economic demand, both in the same location, have created a unique logistics advantage. By manufacturing and consuming in the U.S., both shipping costs and emissions can be greatly eliminated. If pursued and supported, these advantages will continue to be the key to further creating and re-shoring manufacturing and thus creating millions of high wage manufacturing jobs. Proper steps can help promote and facilitate this incredible opportunity.

![]()

October 2020

www.shalecrescentusa.com

Contact Info: Greg Kozera at (304) 545-7259 or gkozera@shalecrescentusa.com

![]()

The Independent Petroleum Association of America (IPAA) has been committed to sustainability efforts through our vision, strategy and approach to Environmental, Social and Governance (ESG) priorities.

This week IPAA is formally launching our new ESG Center. We’ve partnered with FTI Consulting, a global business advisory firm with expertise in ESG issues, to offer our members this new resource. FTI has long partnered with IPAA and our members to effectively advocate for the industry and communicate on complex issues, including on IPAA’s Energy In Depth and Energy Tax Facts projects. We are excited to work with them on this important effort to provide support for members as they look to understand this growing trend and develop ESG programs that align with their unique business strategies and stakeholder needs.

From our ESG Center we plan to share resources with information on the growing necessity of ESG programs and how to build an authentic and effective program, future virtual and in-person educational events, our current partnerships, and more. Just yesterday, we held our first webinar on ESG issues: “How to Build An Authentic ESG Program.” The webinar covered topics including addressing misconceptions, where to start, and best practices. You can find links to view the full recording of the webinar and the slidedeck that was used here.

Some IPAA member companies have established ESG programs and others are just looking to get their foot in the door. Our aim is for the resources we share to be helpful to both groups and everyone in between. ESG programs are not just a large public company issue or concern. There are a variety of drivers – in the investor world you have players like BlackRock and StateStreet, ESG ratings agencies, etc., but you also have Private Equity increasingly looking at ESG, including some funds appointing staff to oversee ESG.

ESG is also as much about mitigating risk as it is about capturing opportunity. At IPAA we know all the efforts underway at our member companies to support a safe workforce, protect the environment, and commit to our communities. An authentic ESG program both aggregates and invests in these areas but communicates about them in a way that safeguards your company’s reputation, and enhances your social license to operate.

Stakeholder demands are growing. As ESG becomes even more integral to financial performance and investor expectations, an organization’s approach to ESG will only grow in importance as well. In such extraordinary, uncertain and unsettling times, oil and natural gas producers’ effective management of ESG will contribute to sustainable business resilience.